》View SMM Copper Prices, Data, and Market Analysis

》Subscribe to Access SMM Historical Spot Metal Prices

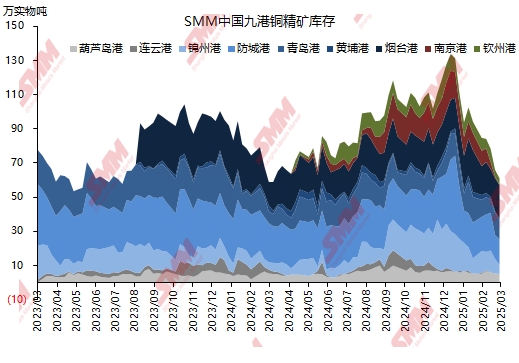

At the end of last year, driven by the need for winter stockpiling and market share competition, Chinese smelters significantly accumulated copper concentrate raw material inventories. Specifically, by the end of December 2024, SMM copper concentrate inventories at nine ports reached 1.31 million mt, primarily concentrated at Jinzhou Port (mainly serving smelters in north-east China and Inner Mongolia), Yantai Port (mainly serving smelters in Shandong), Fangchenggang (mainly serving smelters in south-west China), and Nanjing Port (mainly serving smelters along the Yangtze River basin).

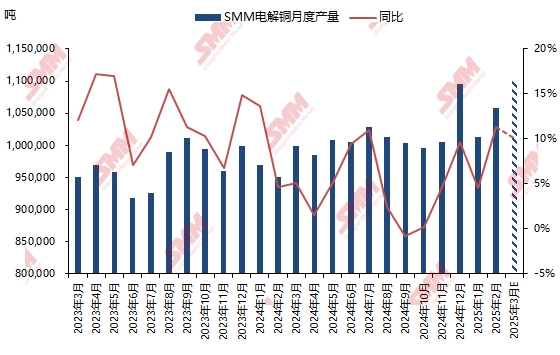

With the increase in China's copper cathode capacity and the rising production targets of smelters, copper concentrate inventories, the primary raw material for copper cathode, have been rapidly depleted. Although port inventories of copper concentrates cannot fully represent the supply-demand balance of copper concentrates in China, SMM's nine-port copper concentrate inventories dropped from the peak of 1.31 million mt at the end of last year to 610,000 mt by early March 2025. This represents a reduction of more than half within less than a quarter, a remarkably fast pace. Supporting this trend is the record-high monthly production of copper cathode in China, as reported by SMM. Meanwhile, the smelting volume of secondary copper, another raw material for copper cathode, has not seen a corresponding increase. According to SMM estimates, the monthly smelting volume of secondary copper is around 160,000-170,000 mt in metal content. Additionally, the implementation of domestic reverse invoicing policies and concerns over the impact of the China-US trade war on imported secondary copper supply have exerted pressure on both domestic and overseas secondary copper supply chains.

SMM expects that as China's monthly copper cathode production continues to rise, the total contribution of secondary copper smelting to copper cathode production may continue to decline, with its contribution ratio decreasing. In contrast, the contribution level of copper concentrate raw materials to copper cathode production is expected to increase, implying a continued reduction in copper concentrate port inventories.

》Click to Access the SMM Copper Industry Chain Database